Invesco QQQ (NASDAQ:QQQ), the Nasdaq-100 ETF heavy with tech stocks, is up 40% year-to-date despite a promise of at least two more rate hikes in 2023. Many investors celebrated the return of the tech bull market. One think tank economist declared, “Ladies and Gentlemen, the recession has been canceled!” on June 29th.

Not so fast.

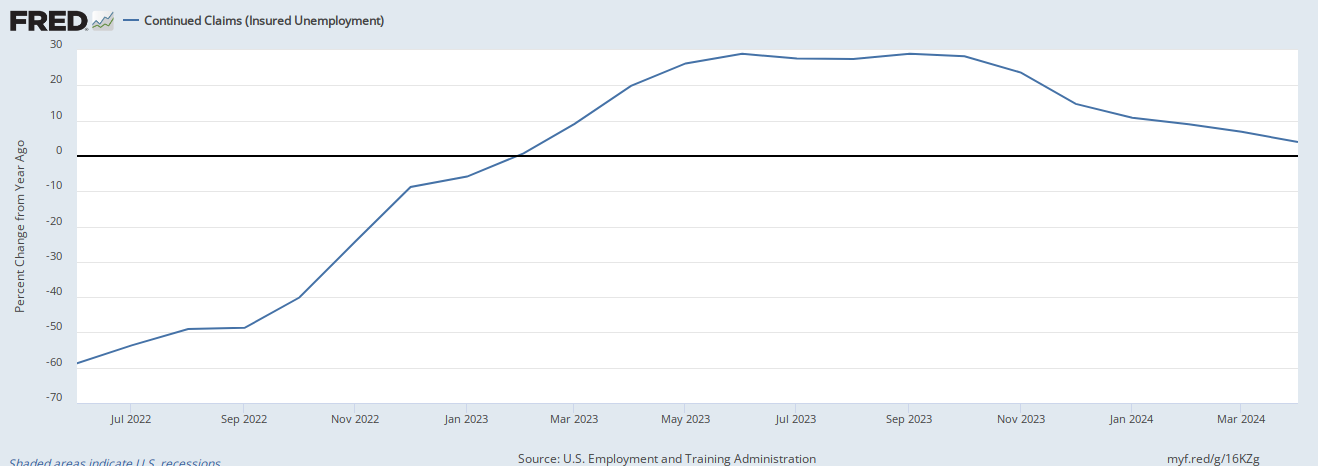

Inflation is down to an almost-respectable 4%. Still, other recession indicators, like the continued claims report, indicate a near-inevitable recession. Continued claims, which track consecutive unemployment rates, have historically been linked to recessions when they surpass 20%. As of today, we have surpassed that threshold, currently standing at an even 30% in April.

{kind=link}

Recession aside, little has changed in monetary policy to imply a return to the cheap debt era that fueled much of tech’s growth. Worse, these three tech stocks have systemic risks threatening their stock price – and the market hasn’t yet priced them in.

To avoid the tech stock crash, investors should take their gains off the table and sell these tech stocks in July.

Apple (AAPL)

Apple (NASDAQ:AAPL) is a juggernaut amid tech stocks. Gaining more than 50% since January, Apple just blew past the $3 trillion market capitalization mark.

But even with an improved economy, that valuation reversal doesn’t seem practical. Below the surface, concerning issues may spell trouble for Apple.

First, supply chain woes are rearing their head as Apple reported production forecast cuts to its mixed-reality headset, the Vision Pro. The product doesn’t launch until next year, but early signs point to trouble. Yes, the initial launch primarily targets developers instead of consumers. And, yes, the revised forecast represents a fraction of Apple’s overall revenue projections.

Slashed production highlights critical risk for Apple, reliant on tight supply chains and shipping routes. Apple’s risk of unpredictable disruptions compounds when considering the geopolitical effects on some of its key production partners.

Recent news also points to something rotten within Apple’s consumer banking initiatives. Despite the recent launch, partner Goldman Sachs (NYSE:GS) is reportedly seeking an offramp from their joint high-yield savings venture. While more of a Goldman problem, turbulence in Apple’s attempt to diversify revenue streams remains troubling – particularly as its recent buy now/pay later initiative begins gaining traction. Short-term consumer loans’ tight profit margins could cause Apple to overextend quickly.

The resumption of student loan payments raises concerns about Apple sales. 34% of adults age 18-29 that hold student debt, and this demographic represents a significant portion of Apple’s customer base. Additionally, as consumers deplete their excess savings, there is a possibility of reduced spending on Apple’s core offerings.

Even if bullish on Apple in the long term, July might be the time to realize gains before this tech stock crashes.

Snap (SNAP)

Snap Inc (NYSE:SNAP), better known as Snapchat, is up 35% since January, with little to justify the increased valuation. Although daily active user counts continue rising, Snap’s done little with the market data collected and monetization of the platform. In Snap’s most recent quarterly filing, the company reported a 7% drop in revenue alongside a 4.5% cost of revenue. Unprofitable for each of the past four years, Snap’s window to monetize its customers may have closed.

Snap’s primary risk is the depth of its competitive pool. Meta (NASDAQ:META) may have a relatively flat daily active user growth on its cornerstone service, Facebook. However, its diversification across Instagram, Messenger, Facebook Marketplace and even its metaverse initiatives point to a landscape challenging to exit for consumers. With no such fence or moat surrounding Snap’s product, it faces the constant risk of consumer capture from other, more diversified firms.

Despite executive assurance to the contrary, Snap’s best bet may be angling for an acquisition. In the meantime, investors may want to jump ship before it sinks.

Block (SQ)

Formerly known as Square, payment processing provider Block Inc (NYSE:SQ) has remained relatively flat since January despite a 16% overall market gain over the same period. While a March short report weighed heavily on the firm, Block’s rebounded since then. But a new entrant poses a significant obstacle to Block’s primary mission “to make commerce and financial services easy and accessible.”

That entrant is the Federal Reserve.

FedNow, the Federal Reserve’s instant payment system, is set to roll out in July. Initial customers are primarily institutional banking firms seeking respite to legacy processing and clearing systems. Per the Federal Reserve, though, FedNow’s goal is to increase liquidity and payment processing speed for a range of small businesses and employees, including “gig economy” workers, with an infrastructure enabling financial transfers in as few as 10 seconds. Eventually, FedNow aims to enable peer-to-peer transactions, much like Block’s CashApp service. Between peer-to-peer market capture and surrendering small business clients to FedNow, Block is now racing against the Federal Reserve.

And, if the past few years taught us anything, it’s don’t bet against the Fed.

On the date of publication, Jeremy Flint held no positions in the securities mentioned. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.